Why now

Imagine an investment that will continue to grow passively without the daily grind and headaches!

~ Let Us Show You How Massive the Opportunity In The After-Foreclosure Real Estate Sector Is... ~

First, Let's Look at What's Coming

Do You Remember the Housing Crash of 2007-2008?

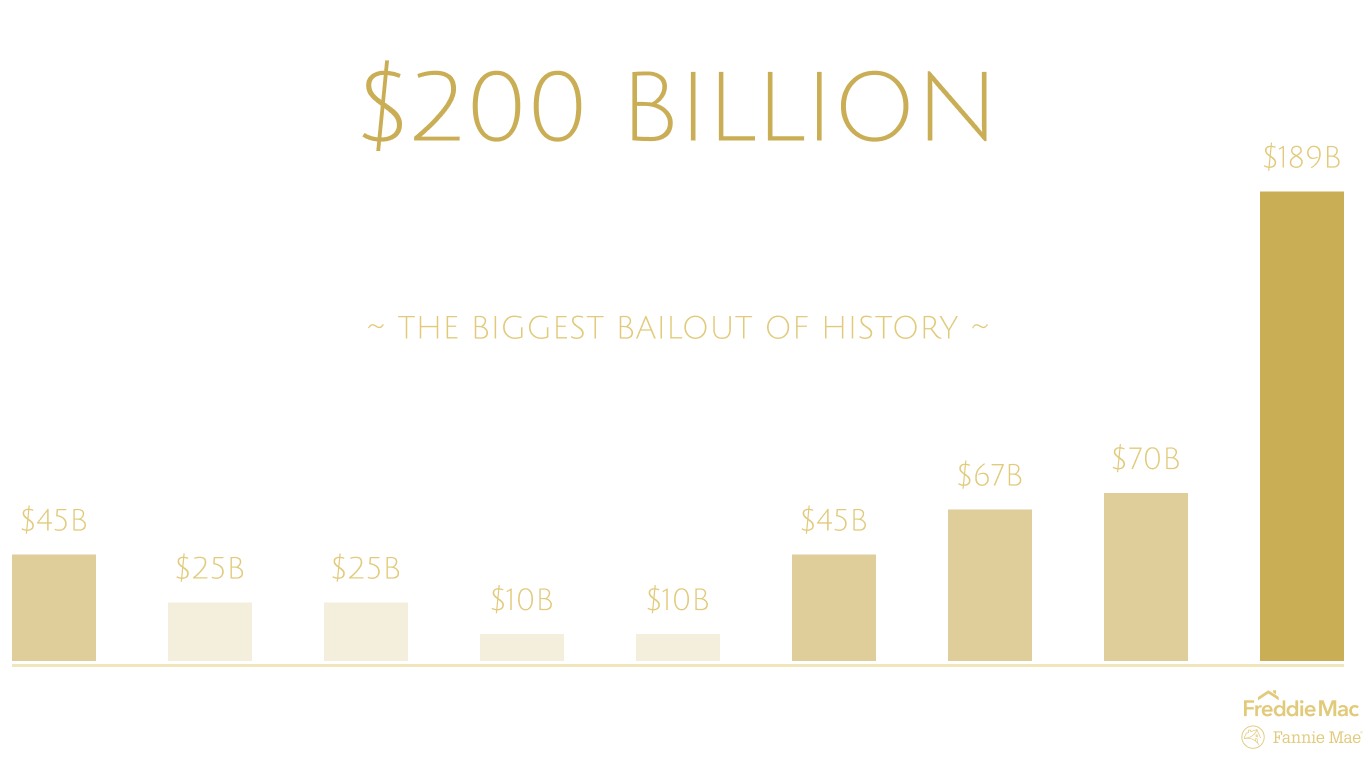

You know what we’re talking about. It wasn't called the housing crash; it was called the government bailout of huge financial companies such as AIG and Goldman Sachs.

So, why are we bringing up old stuff?

THE BIGGEST BAILOUT IN U.S. HISTORY

Simple: it completely disrupted and destroyed housing and financial markets.

The housing boom made fortunes and then destroyed it.

Who knew that huge banks such as Citi, Wells Fargo, and Bank of America would be on the brink of going out of business, opening up a scenario in which the entire world financial system could collapse?

Economist David Malpass argued that the housing market was healthy and that much of the rise in prices simply represented a "catch-up" because they had lagged behind the increase in equity prices since the mid-1990s.

The Bear Stearns report also noted: rising household formations, declining unemployment, low-interest rates, a decline in the inventory of unsold homes, and the 1997 cut in capital gains taxes on owner-occupied homes as other reasons for its continued optimism.

HOUSING MARKET EXPECTED TO LEVEL OUT IN 2006

Why Housing Couldn’t Crash

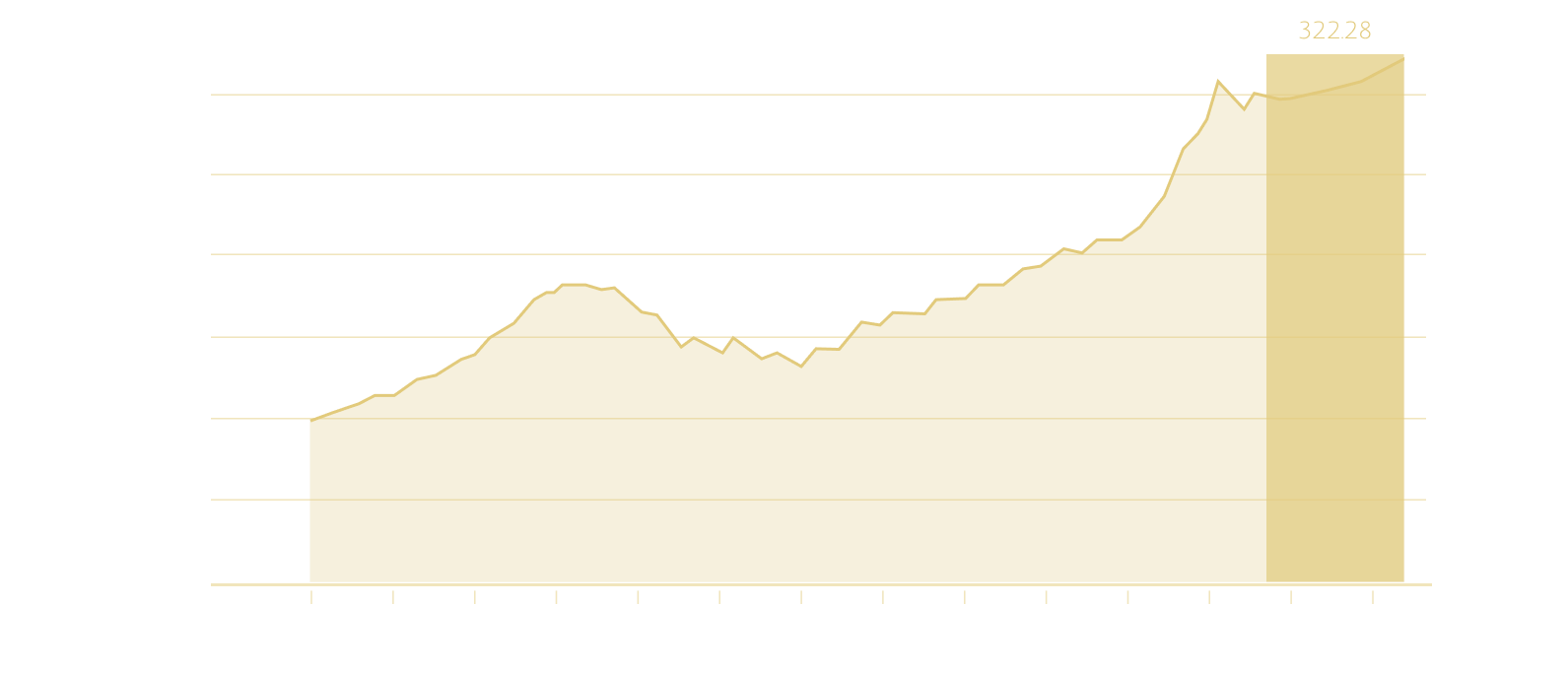

where goldman sachs expects u.s. home prices to go through 2026

We all know how this story ended . . .

Stop! The Pending Foreclosure Crisis is Here.

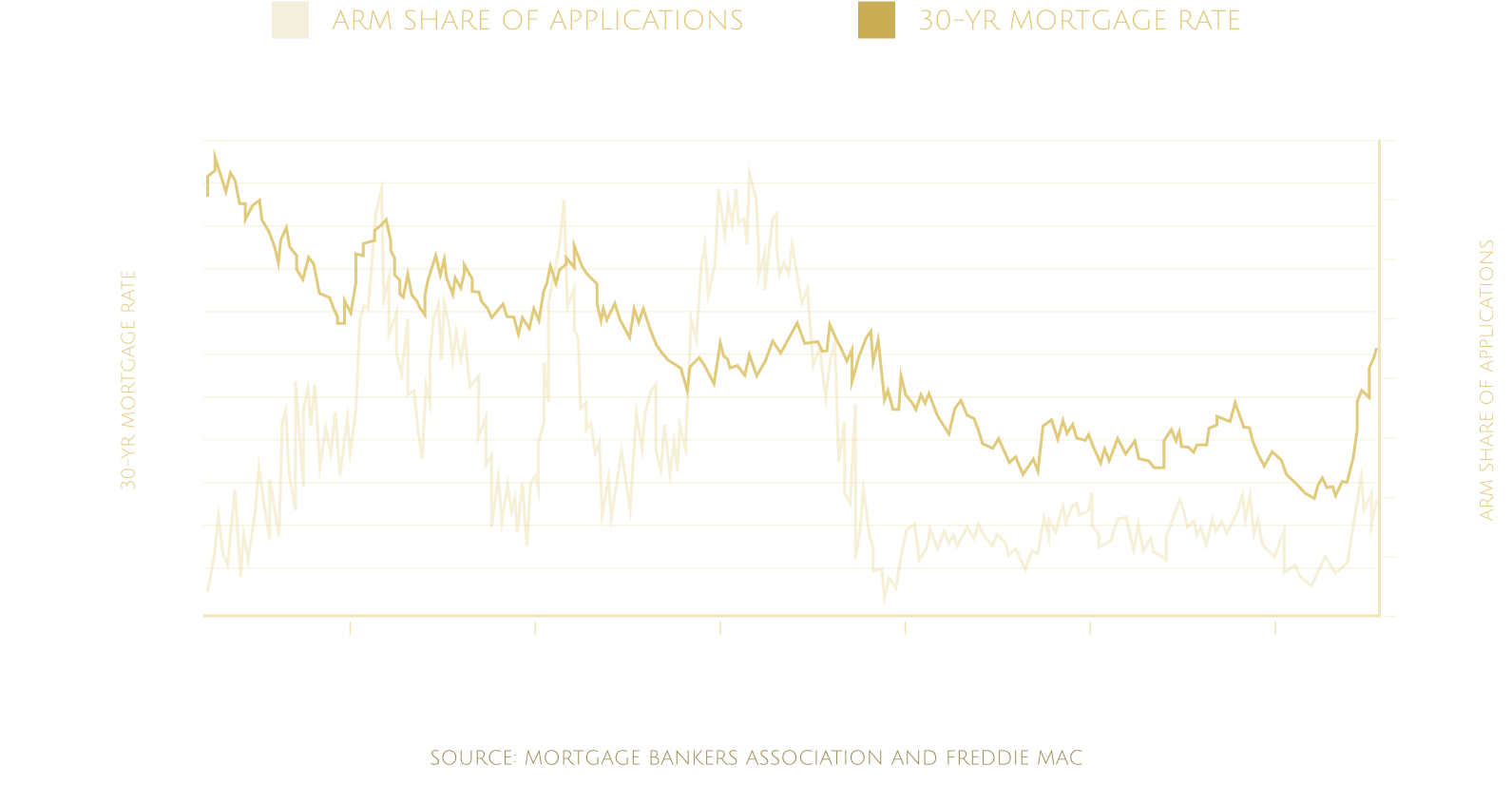

Over the last eight years, adjustable-rate mortgages (ARMs) have gained popularity, enabling buyers to afford more expensive homes with their budgets.

Share of arms vs mortgage rates

Now, with the introductory period of many adjustable-rate mortgages (ARMs) ending over the next few years, monthly mortgage payments are projected to rise significantly, from $1,000 to $2,300.

Here is an excerpt from an article by NBC from June 9, 2023:

“A new study shows home foreclosures in California are up more than 20% from this time last year.

The California numbers follow a nationwide trend and are the second highest of any state in the country, but they are nowhere near the number of foreclosures seen during the 2008 crash.

Part of the reason many are defaulting on the mortgage loan is the adjustable rate mortgages that have shot up suddenly after the recent rise in interest rates.”

RISKY MORTGAGES COULD LEAD TO FORECLOSURE SPIKE

The article's point was that home buyers seeking adjustable-rate

mortgages in this high-rate environment could be at an increased risk of foreclosure...

"The Mortgage Bankers Association found that applications for 5/1 adjustable-rate mortgages (ARMs) climbed 32.5 percent in the week ending October 6 as loan rates fell to the mid-6 percent range.

Meanwhile, the total number of ARM applications surged 15 percent last week, and in what has been the highest percentage since November 2022, borrowers who were looking for an adjustable-rate mortgage (ARM) made up 9.2 percent of the entire group."

In the memo, Mortgage Bankers Association Deputy Chief Economist Joel Kan explained a bit about how he saw this affecting foreclosures."

The yield curve has become less inverted in recent weeks, and ARM pricing has certainly improved.

This could lead to a spike in foreclosures in the future as ARMs are generally far riskier than traditional 30-year fixed-rate mortgages. The reason is that while traditional mortgages will stay the same no matter the year, an ARM changes after the introductory period to reflect current rates.

Sometimes, borrowers plan for rates to drop after the introductory period, while other times, they don't expect to own the home for long. Still, occasionally, homeowners are punished for choosing these riskier options when mortgage rates rise, and they are forced to pay a higher amount.

Anyone who took out an ARM before the COVID-19 pandemic, for example, and did not take the opportunity to refinance while rates were at the lowest point in history, is right to have regrets."

An avalanche was sure to be building underneath. But what stopped the downfall?

Ummmmm, something called the pandemic... have you heard of it??

COVID-19 has touched every part of the world, primarily because it had stopped the flow of income, spending, and money.

Mortgage payments were no different.

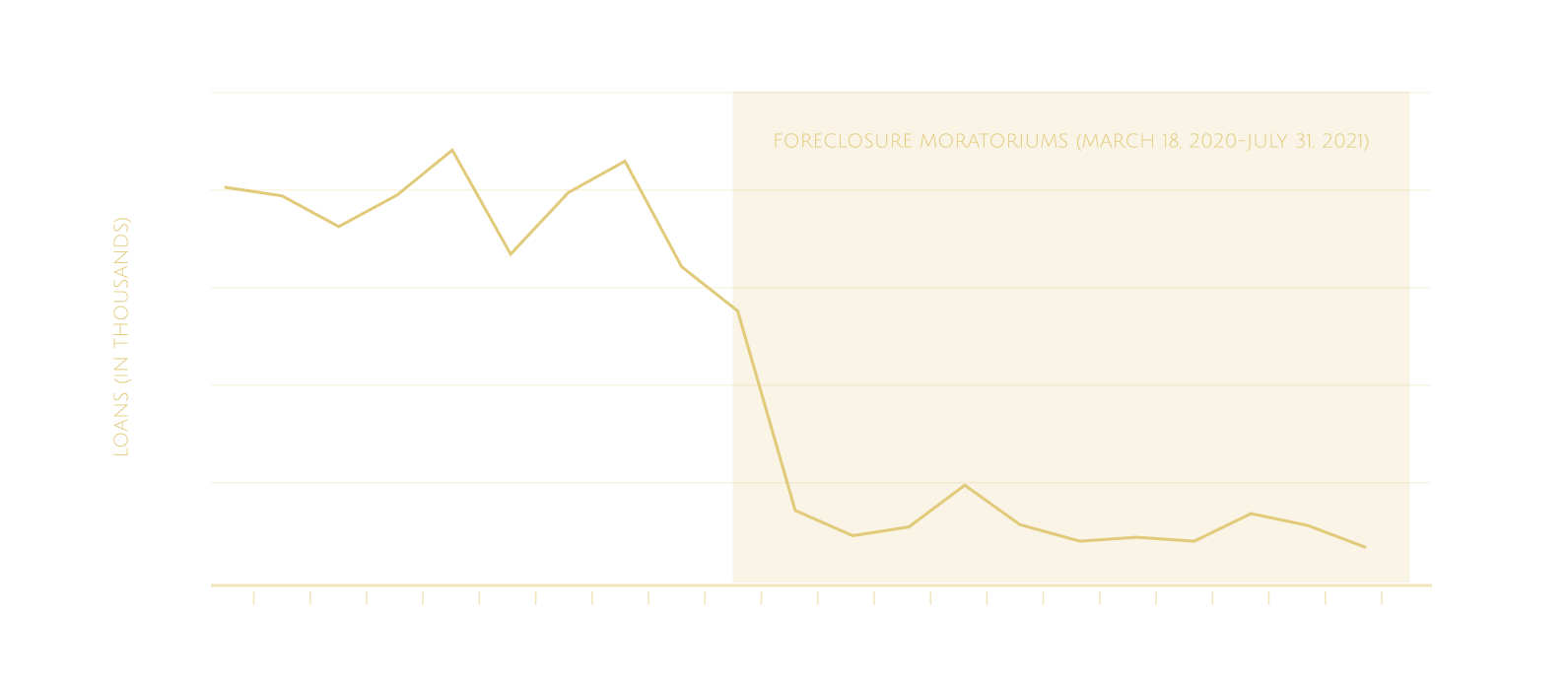

In fact, 3.4 million homeowners paused their payments in May 2020

(according to the United States Government Accountability Office).

When the CARES Act was announced, millions more received relief from possible foreclosures.

Foreclosures were paused.

The pandemic disrupted nearly every industry, leaving some irrevocably changed. We've all witnessed its devastating impact on retail, education, and the restaurant industry.

But the pandemic didn't stop there

It completely destroyed small businesses and their employees.

According to the Small Business Administration, small businesses employ 46.4% of the private sector employees.

Millions of businesses closed and never reopened.

these businesses made it through the hardest part of the pandemic. then they closed.

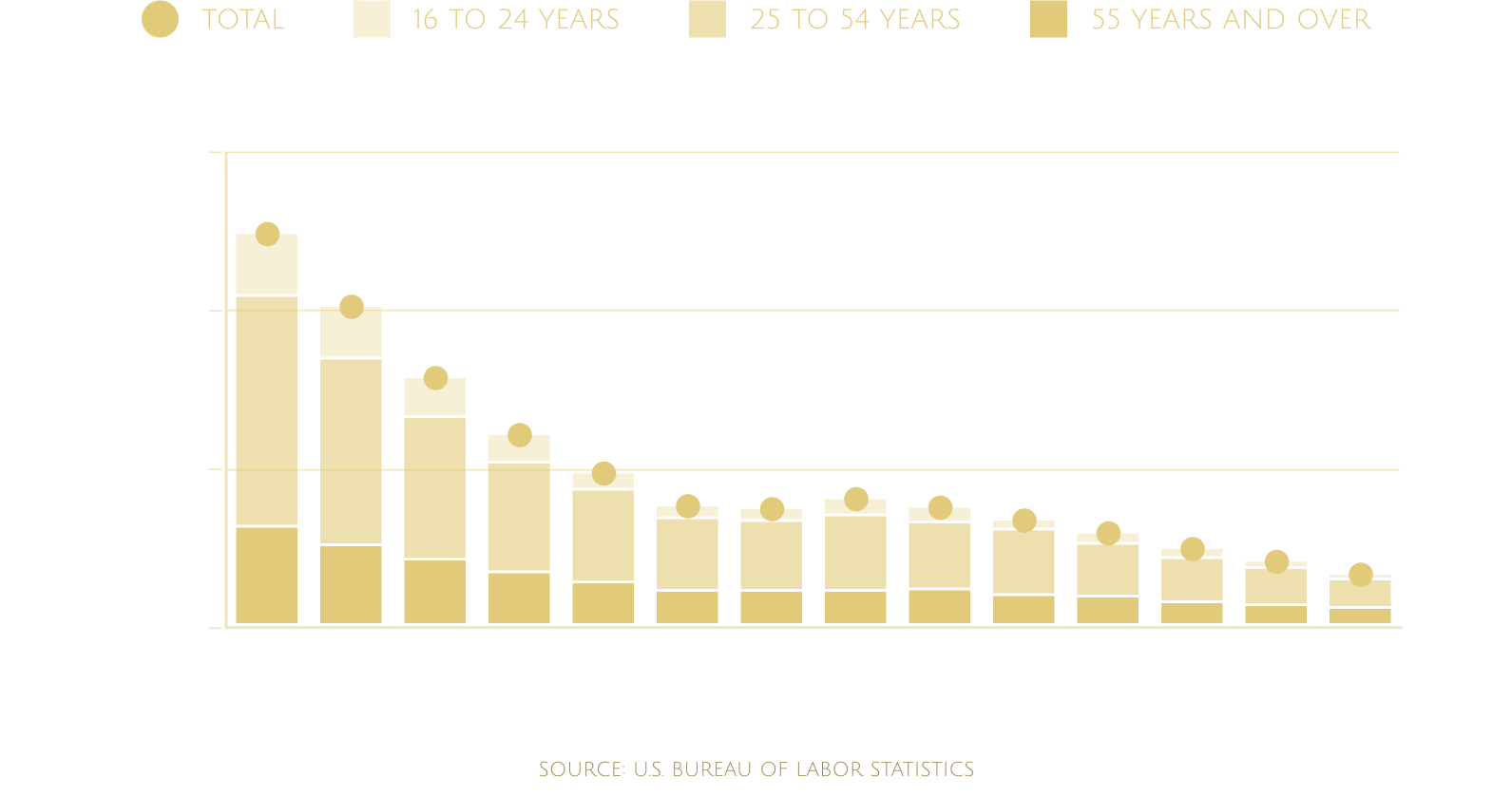

6.2 million people were unable to work because their employers closed or lost business due to the pandemic

It unfolded right on Main Street. First, bars and restaurants—central to community life and social interaction—were hit hard.

Then, the ripple effect reached warehouse businesses that supplied these establishments, eventually impacting personal service-based companies as well.

Underwater properties are at their lowest since the Great Depression

The major banks, mortgage companies, and large financial institutions view this period as a once-in-a-century opportunity.

Selma Hepp, Chief Economist for Corelogic, had this to say:

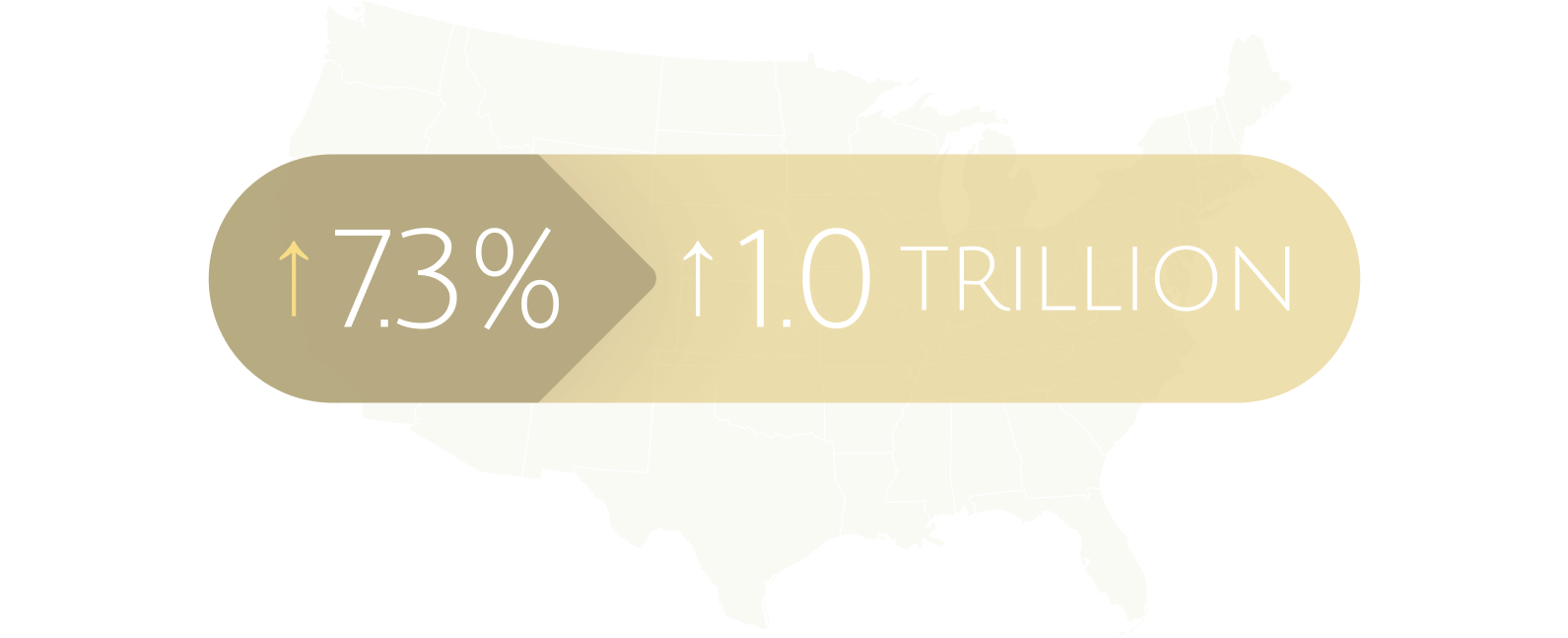

“While equity gains contracted in late 2022 due to home price declines in some regions, U.S. homeowners on average still have about $270,000 in equity, nearly $90,000 more than they had at the onset of the pandemic.

even in idaho, where borrowers were the most vulnerable to losses, the typical homeowner with a mortgage still has about $250,000 in remaining home equity”

national homeowner equity

HOMEOWNER EQUITY KEEPS GROWING AROUND U.S. IN THIRD QUARTER DESPITE HOUSING MARKET SLOWDOWN

FORECLOSURES SPIKE AS BANKS LOWER THE BOOM ON HOMEOWNERS

Banks brutally and aggressively started to pounce on this new found money.

After the payment freeze period from the COVID-19 foreclosure moratorium, which by law paused millions of active foreclosures for 18 months, the forbearance amount immediately became due on millions of mortgages.

According to real estate data provider ATTOM, lenders repossessed nearly 96,000 properties during the first three months of 2023, up 22% from the same period in 2022.

The lenders have little reason to work with borrowers when they can immediately recover the entire loan amount plus interest and fees at a foreclosure action.

The greed of these banks and mortgage companies escalated so rapidly that the government had to intervene once again.

WASHINGTON — Helping Veterans and their families stay in their homes is a top priority at VA. Over the past year, we’ve been able to help more than 145,000 Veterans and their families retain their homes and avoid foreclosure. Even in the dynamic housing market of the last several years, rates of foreclosures of VA-backed mortgages are among the lowest in the country. And at the same time, we know that there are still Veterans struggling to make their payments.

To ensure these Veterans can stay in their homes, we are taking two steps:

This is a deeply troubling and often overlooked trend unfolding beneath the surface of America.

Most people worldwide feel disillusioned with the current financial systems, perceiving them as rigged against the average person. It has become increasingly difficult to get ahead, as each dollar stretches less than it did just a few years ago.

So, what do we do?Do we sit idly by and watch this unfold?

Do we turn a blind eye and ignore the plight of those impacted?

These are the critical questions we must ask ourselves as we navigate this challenging reality.

No! We Help! We Fight For The People!

We can’t reverse the foreclosures already taking place.

However, what we do is step in and help those affected emerge as winners from an otherwise tragic situation.

The Trifecta Opportunity: Adjustable Rates Mortgages, Lost of Incomes, and Home Equities Increasing

The opportunity for us is unbelievably massive.

Let’s look at why all of this makes sense:

It is a simple concept to understand.

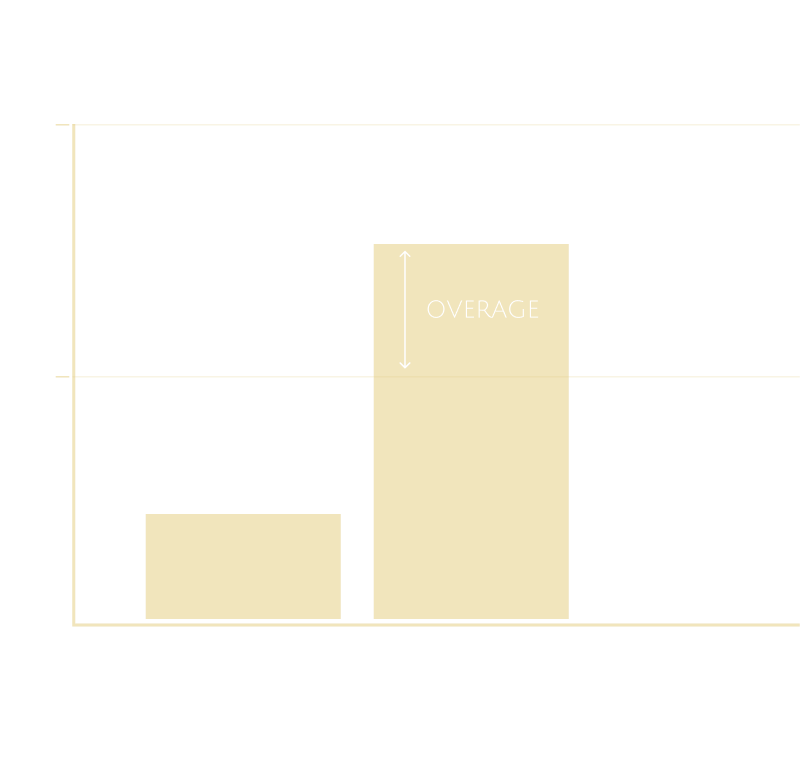

When the government executes a foreclosure auction and the sale creates an amount larger than the amount owed to the lender, this amount is called an “overage.”

Here is an example:

Someone owes the bank $120,000.

The home is sold at a foreclosure auction for $300,000.

That $300,000 remains in the government’s bank account. It doesn’t matter if the homeowner has paid off 29 years of a 30-year mortgage—the bank will still initiate foreclosure after just three missed payments.

The additional $180,000 is referred to as the overage. The individual who was foreclosed on retains legal rights to claim these funds, typically within a window of three months to two years, depending on state regulations.

After that period expires, the overage amount is automatically forfeited to the local government entity.

THE GOVERNMENT

SEIZES THE FUNDS

Here are three examples of the state laws mandating the distribution:

2023 California Code

Revenue and Taxation Code - RTC

DIVISION 1 - PROPERTY TAXATION

PART 8 - DISTRIBUTION

CHAPTER 1.3 - Distribution of Proceeds From Sale of Tax-Deeded Property

Section 4675.

4675. (a) Any party of interest in the property may file with the county a claim for the excess proceeds, in proportion to that person’s interest held with others of equal priority in the property at the time of sale, at any time prior to the expiration of one year following the recordation of the tax collector’s deed to the purchaser. The claim shall be postmarked on or before the one-year expiration date to be considered timely.

2022 Texas Statutes

Tax Code

Title 1 - Property Tax Code

Subtitle E - Collections and Delinquency

Chapter 34 - Tax Sales and Redemption

Subchapter A. Tax Sales

Section 34.04. Claims for Excess Proceeds

Sec. 34.04. CLAIMS FOR EXCESS PROCEEDS. (a) A person, including a taxing unit and the Title IV-D agency, may file a petition in the court that ordered the seizure or sale setting forth a claim to the excess proceeds. The petition must be filed before the second anniversary of the date of the sale of the property. The petition is not required to be filed as an original suit separate from the underlying suit for seizure of the property or foreclosure of a tax lien on the property but may be filed under the cause number of the underlying suit.

2023 Florida Statutes

Title XIV - Taxation and Finance

Chapter 197 - Tax Collections, Sales, and Liens

197.582 - Disbursement of Proceeds of Sale.

197.582 Disbursement of proceeds of sale.—

(1) If the property is purchased by any person other than the certificateholder, the clerk shall forthwith pay to the certificateholder all of the sums he or she has paid, including the amount required for the redemption of the certificate or certificates together with any and all subsequent unpaid taxes plus the costs and expenses of the application for deed, with interest on the total of such sums for the period running from the month after the date of application for the deed through the month of sale at the rate of 1.5 percent per month. The clerk shall distribute the amount required to redeem the certificate or certificates and the amount required for the redemption of other tax certificates on the same land with omitted taxes and with all costs, plus interest thereon at the rate of 1.5 percent per month for the period running from the month after the date of application for the deed through the month of sale, in the same manner as he or she distributes money received for the redemption of tax certificates owned by the county.

Unfortunately, Attorneys

are Needed . . .

After-foreclosure real estate is an extremely obscure aspect of law, real estate, and the court system.

To have these funds released, an attorney is typically required to navigate the legal process and sue the government entities involved.

That’s crazy, right?

It gets even crazier because some states, such as Texas, impose strict limits on how much an attorney can charge for these cases. In Texas, attorneys are capped at charging no more than$1,000.

What attorney is going to work for that??

Exactly. None.

The government has made it nearly impossible for individuals who have faced the tragedy of foreclosure to access the funds they are rightfully owed, burdening them with endless regulations and the necessity of legal representation.

How can someone who has just endured the financial hardship of a foreclosure possibly afford an attorney?

They can’t, right?

What Could You Expect?

Number of Capital cycles in a year

We succeed when

you succeed.

Here's What You Need

To Do Right Now.

This presentation for Milan CM AF RE Fund LLC and any accompanying appendices or exhibits (the “Presentation”) has been prepared by Milan CM AF RE Fund LLC for informational purposes only. This Presentation is confidential and intended solely for its designated audience. Recipients of this Presentation may not reproduce, redistribute, or pass on, in whole or in part, whether in writing, orally, or in any other format, this Presentation or any of the information contained herein.

This Presentation does not constitute an offer to sell or a solicitation of an offer to purchase limited partnership interests or any other securities. Any prospective investor is strongly advised to carefully review all private placement memorandum and subscription documents (“Investor Documents”) and consult their legal, financial, and tax advisors before considering any investment in Milan CM AF RE Fund LLC.

Past performance is not indicative of future returns or results. Furthermore, there is no guarantee of future deal flow.

Certain statements in this Presentation, including those containing words such as “targets,” “believes,” “expects,” “intends,” “estimates,” “projects,” “predicts,” “anticipates,” “plans,” “pro forma,” and “seeks,” as well as similar terms, are forward-looking statements. These statements are not historical facts but reflect Milan CM AF RE Fund LLC’s views and assumptions as of the date of this Presentation regarding future events and performance. All forward-looking statements involve risks and uncertainties, and actual results may differ materially. Key risk factors are detailed in the “Risk Factors” section of Milan CM AF RE Fund LLC’s confidential private placement memorandum.

Important Considerations:

An investment in Milan CM AF RE Fund LLC involves risk. Numerous factors could result in materially different actual results, performance, or achievements than those expressed or implied in this Presentation. Should one or more of these risks materialize, or if the underlying assumptions prove incorrect, actual outcomes may vary significantly.

Milan CM AF RE Fund LLC and its members, officers, directors, owners, employees, agents, representatives, suppliers, and service providers provide this Presentation and any related materials for informational purposes only. By engaging with this material, you agree to our Terms of Use and Privacy Policy. Please review these carefully. By using this material, you agree not to hold Milan CM AF RE Fund LLC, its affiliates, or any third-party service providers liable for any claims arising from decisions made based on this information.

Neither Milan CM AF RE Fund LLC nor its affiliates are registered investment advisors or broker-dealers. They do not provide tax or financial advice and do not guarantee any specific tax or financial outcomes.

Nothing in this Presentation constitutes an offer to sell securities. Any such offer will be made solely through a separate Private Placement Memorandum or Offering Circular, dependent on the targeted fund. This Presentation provides a general overview of the business, various funds, and the purpose and principal terms of investment. All summaries are qualified in their entirety by the detailed information contained in the Private Placement Memorandum.

DISCLAIMER:

Potential investors should request a copy of the private placement Memorandum for review before investing. The content provided herein is for informational purposes only and does not constitute an offer to sell or solicit the purchase of securities. Any such offer is extended solely to accredited investors through the confidential private placement memorandum, which includes material information about the fund’s investment strategies, terms, and risks.

All content on this website is protected by copyright law. Unauthorized use or reproduction of this content in any form is strictly prohibited. Redistribution, copying, or other use of this material without the express written consent of the copyright owner is not permitted.

© Copyright 2025 MCM LLC - All rights reserved